If you’re under 35 and haven’t bought a house yet, you’ve probably felt the weight of it. Not just the financial pressure, but also the cultural expectations. The nagging sense that you’re falling behind an invisible adulting schedule. Your parents did it, your boss has done it, so why does it feel like the door to home-ownership has quietly slammed shut on you?

If this sounds familiar, you’re not alone. For young Brits today home-ownership isn’t just a dream, it is practically an extreme sport and not because they’re lazy or over caffeinated. ( though let’s be honest, coffee is excellent) It’s because the truth is more complicated than “just save harder” or stop “buying takeaway,” the rules have changed and the housing market has become a maze of high prices, low wages and sacrifice.

Let’s unpack what is going on, there’s nuance to this crisis, real stories, real strategies and real experts willing to cut through the noise. Like Henry Pryor, a longtime housing insider who has seen every twist in the tale.

I spoke to Henry Pryor about what’s really going on, and what needs to change if this generation is going to have any shot at a front door with their name on the letterbox.

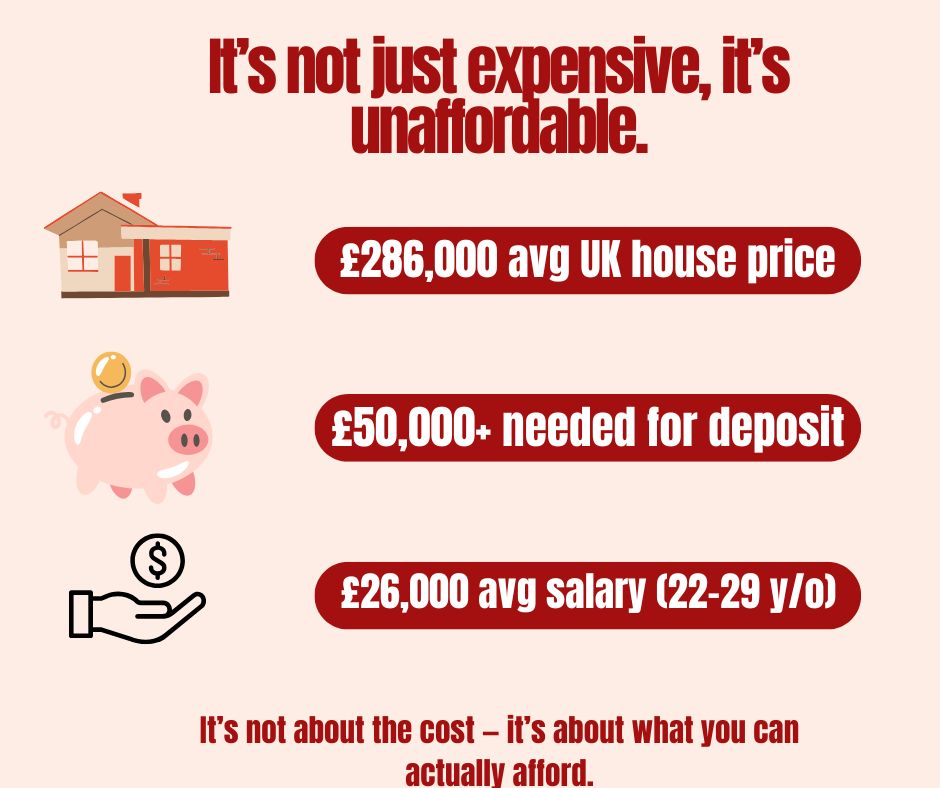

It’s not just expensive, it’s unaffordable:

Property expert Henry Pryor has seen every twist and turn of the UK housing market. But even he admits that something fundamental has shifted. He said buying a house is: “Much more expensive and they’re also as a result much more unaffordable. Affordability is the biggest problem for first time buyers in particular, but for younger generations going forwards.”

The distinction matters, it’s not just about sticker prices, it’s whether young people can realistically bridge the gap between earnings and ownership.

The average UK house price is around £286,000. In London, it’s over £500,000 and the average salary for a 22-29 year old in the UK? Roughly £26,000, according to the ONS. To afford a modest home, you’d need a deposit of £50,000+ and a mortgage most lenders wouldn’t give without a much higher income or help from parents. ( also known as the bank of mum and dad)

Mr Pryor also acknowledges the generational shift and doesn’t romanticise the past, he said: “Investing in property which is what has happened over the 25 years has been seen as asset drive as opposed to a home and has driven up the cost of property and made it less affordable because people have seen it as a vehicle to plan for their retirement.”

But here’s the thing: homes were never meant to be pension plans. They’re supposed to be a shelter. A place to build a life, not a portfolio. Yet for decades, housing policy has treated property as an investment vehicle first, and a basic human need second. The result? A system that rewards hoarding and speculation, while locking out entire generations.

It’s the market even meant for first time buyers anymore?

It’s a fair question and according to Mr Pryor, one with a fairly stark answer. He explained that : “first time buyers are really important for the lifespan of the housing market, without them the housing market will fall over. 60% of mortgages are taken by first time buyers, so they’re key to the housing market.”

However, despite their importance first-time buyers are increasingly being pushed to the margins of a system that depends on them. Pryor points to a growing imbalance: while these buyers remain vital to keeping the market moving, they’re often the least equipped financially and structurally to compete in it. In short, you might feel like all the cards are stacked against you

Mr Pryor lays it out clearly: today’s first-time buyers aren’t just contending with rising prices or stricter lending criteria, they’re also operating in a market crowded with competitors who often hold a major financial advantage.

He explained that “in capitalism if someone makes me money, someone has to lose that’s how it works, there’s always a victim. For example, if you’re watching David Attenborough on a Sunday morning, we tend to think what a wonderful creature the lion is and we don’t spend nearly enough time worrying about the zebra.”

It’s a striking image, and one that lands hard, because for many young buyers, that zebra is uncomfortably familiar.

In today’s housing market, first-time buyers are often the most vulnerable party in the deal. They’re trying to get a foothold with borrowed money, minimal savings, and no margin for error. Meanwhile, they’re competing with overseas investors, buy-to-let landlords, and second-home owners, all armed with cash, equity, and an appetite for returns.

This is the hard truth: the system isn’t designed for them. It’s designed for efficiency, profit, and risk management. If you’re less profitable, you’re less desirable. That’s not a moral failure, it’s structural design. The result? A generation boxed out, not because they’re doing anything wrong, but because they’re not built to win a game that was never meant for them.

Real people, real stories:

You don’t have to look far to find stories that show just how uneven this playing field really is. On Reddit, young people are sharing what it actually takes to get a foot on the property ladder, and it’s rarely as simple as just “saving harder.”

One Reddit user explains: “ housing is expensive, wages are low. Rent is extremely high and takes a large portion of young people’s salaries, so it’s very hard to save up. Even on a ‘good’ salary, it’s very hard to save enough because of rental costs.”

Another user shared what it took to beat the odds: “It’s definitely possible to get a property but you need either luck or to make some hard choices. You either need help from parents or a well-paying job or to make a lot of sacrifices. Personally, I made a lot of sacrifices to be able to buy my first house at 24 (I’m now 29).”

These aren’t rare cases, they’re honest accounts of a generation forced to choose between comfort and security, with little room for both. It’s not laziness. It’s the price of entry.

What now?

Mr Pryor also challenges the idea of home-ownership, he said: “There’s jeopardy in buying a house. It’s not a one-way bet. People will tell your generation that if you hold property long enough, it will always go up in value. But that’s not guaranteed. You should buy a house if you want somewhere to live.”

He also said that for young people to have a shot at climbing the property ladder, the government has to build more houses to meet the growing the demand and ensure affordability.

And that’s the deeper issue. Home-ownership has become a symbol of adulthood, stability, and financial maturity — yet the process of getting there is increasingly unstable, unequal, and high-risk. It demands sacrifice, yes. But it also demands a system that doesn’t treat you like the zebra every time you step into the arena.

Because this isn’t just a market problem. It’s a value problem.

A society that tells young people to work hard and play by the rules, and then offers them a housing ladder with the first rung broken, isn’t just failing economically. It’s failing morally. It’s time we stopped cheering for the lions without asking who’s being trampled underneath.

Mr Pryor doesn’t say the game is rigged, but it’s clear that the odds aren’t exactly even. Until that changes, owning a home will remain less about independence, and more about endurance.

Click on the link If you want more read more about our heinous housing stories.